The gains in TiumBio and DT&CRO are attributed to expectations of improved earnings. Meanwhile Samchundang Pharm(SCD Pharm) continued to decline for a second consecutive day, despite withdrawing its block deal (after hours bulk trade) plan and directly addressing various recent allegations.

TiumBio stock trend on Apr 7.(Image=MP Doctor)

◇TiumBio to Announce Interim Results of Phase 2 Trial on Combination Immunotherapy Next Month

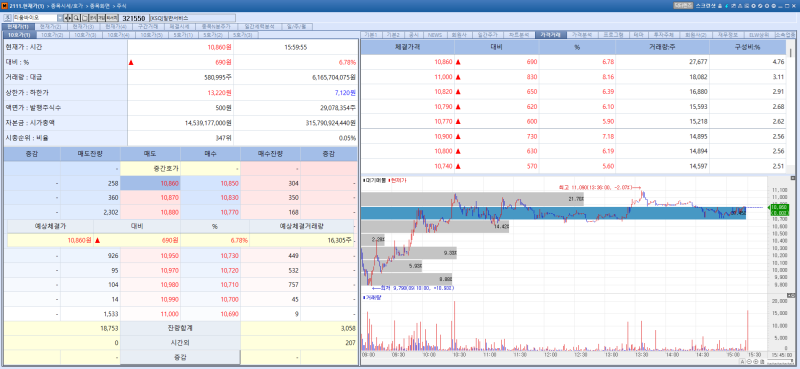

According to KG Zeroin’s MP DOCTOR on the 7th shares of TiumBio rose 6.78% from the previous day to close at 10,860 won. The increase is attributed to expectations surrounding interim results of its immuno oncology drug under development.

TiumBio’s clinical data for its immunotherapy candidate Tofacitinib (TU2218), has been accepted as an abstract for presentation at the American Society of Clinical Oncology 2026 (ASCO 2026) scheduled to be held in the United States this May.

Tofacitinib is a dual inhibition immuno-oncology candidate that simultaneously targets transforming growth factor beta (TGF-β) and vascular endothelial growth factor (VEGF) aiming to improve the tumor microenvironment and enhance response rates to immunotherapy. TiumBio is currently conducting a Phase 2a clinical trial of the drug in both Korea and the United States.

At ASCO 2026, the company will present a poster on the interim results of a Phase 2 trial evaluating Tofacitinib in combination with Merck’s immunotherapy Keytruda for patients with head and neck cancer. Previously at the Society for Immunotherapy of Cancer (SITC) 2025 TiumBio reported a 70.6% objective response rate with partial responses observed in 12 out of 17 evaluable patients.

This time, the company plans to disclose updated data, including additional patients enrolled since July last year, along with extended follow up results. TiumBio is also in discussions regarding the global out-licensing of its endometriosis treatment Merigolix (TU2670).

On a consolidated basis, TiumBio posted sales of 12.3 billion won last year, up 80.9% year-on-year, marking a record high. Its operating loss narrowed to 16.1 billion won, indicating improved financial performance. The company is expected to continue this trend of earnings improvement this year.

A TiumBio official stated, “The company’s drug pipeline and corporate value have been somewhat undervalued by the market. However the market is now beginning to respond more actively to the clinical progress and commercialization potential of our pipeline.”

DT&CRO stock trend on Apr 7.(Image=MP Doctor)

◇DT&CRO is expected to turn to quarterly profit in the second half of the year driven by the aesthetic boom

DT&CRO’s stock price rose 4.04% from the previous day to close at 3,350 won. The gain is attributed to growing expectations for a rebound in its earnings this year.

DT&CRO achieved a significant improvement in performance as orders for non clinical and clinical studies increased amid a recovery in the domestic pharmaceutical and biotech industry since the second half of last year. In particular, the company has been operating its pharmacokinetics and pharmacodynamics (PK·PD) center Korea’s only facility certified under Good Laboratory Practice (GLP) in full scale since last year.

DT&CRO provides a full service CRO platform covering the entire process from non clinical studies to post-marketing clinical trials (Phase IV) as well as consulting.

The company aims to achieve quarterly profitability in the second half of this year, supported by the growing popularity of aesthetics such as hyaluronic acid (HA) fillers, along with increased demand for improved drugs following the government’s price cuts on generic drugs.

DT&CRO posted revenue of 47.8 billion won and an operating loss of 5.6 billion won last year. Revenue increased 32.7% from 36.0 billion won a year earlier, while the operating loss narrowed by 50% compared to 11.3 billion won the previous year. This improvement is attributed to increased orders for non clinical and clinical projects as the pharmaceutical and biotech industry regained momentum.

As of the end of the third quarter last year the company’s order backlog stood at 49.6 billion won up 16% year on year.

DT&CRO has also strengthened its financial position. Earlier this year, it secured an investment of 20 billion won from private equity firm Eugene Private Equity. The funding allows the company to respond more stably to the put option (early redemption right) on its convertible bonds (CB) maturing this month.

A company official said “Investments in key areas such as the PK·PD center were a strategic decision to complete our full service CRO capabilities while delivering short-term results,” adding, “DT&CRO has now entered a phase where past investments are expected to translate into visible growth and performance starting this year.”

SCD Pharm stock trend on Apr 7.(Image=MP Doctor)

◇SCD Pharm Fails to Restore Investor Confidence Shares Fall for Second Straight Day

SCD Pharm’s stock fell 16.2% from the previous day to 519,000 won, extending its decline for a second consecutive session. The continued drop is attributed to the company’s failure to regain investor confidence despite clarifying suspicions surrounding a canceled block deal and allegations of stock price inflation.

The company’s share price had surged from the 240,000 won range at the beginning of the year to as high as 1.18 million won at the end of last month. However it has since plunged sharply, halving to the 500,000 won range in less than a week.

At a press conference held the previous day SCD Pharm addressed various allegations raised against the company. CEO Jeon In seok explained that the planned block deal worth 250 billion won was not intended to sell at a peak price but to cover approximately 233.5 billion won in taxes, including gift and capital gains taxes adding that the plan has been fully withdrawn.

Regarding the recently disclosed 15 trillion won deal with a U.S. partner for oral semaglutide (an obesity treatment), Jeon said “The Korea Exchange prohibits directly stating projected future sales in disclosures prior to product approval in order to prevent potential investor damage.”

adding “Given the product’s strong potential our U.S. partner accepted a highly unfavorable 9:1 profit sharing structure.”

He also addressed concerns over the approval pathway for the oral semaglutide generic stating that it has been recognized by the U.S. Food and Drug Administration (FDA) as a generic version of Wegovy and emphasized that the company would prove its progress through tangible results.

On March 31 SCD Pharm was preliminarily designated as a company subject to sanctions for failure to comply with fair disclosure requirements regarding earnings forecasts. The final decision is scheduled for April 23.

Shares of its subsidiary Optus Pharm also declined. The stock closed at 8,980 won, down 17.24% from the previous day.