ABL Bio’s stock declined as disappointing selling pressure emerged following the final data results from the Phase 2/3 clinical trial of its bile duct cancer treatment, tobevibart (ABL001) which had been out-licensed to Compass Therapeutics in 2018.

NGeneBio’s shares also dropped weighed down by news of a planned capital increase worth 22.4 billion won. In contrast LivsMed drew attention as its stock rose for the fourth consecutive trading day on expectations of improved earnings.

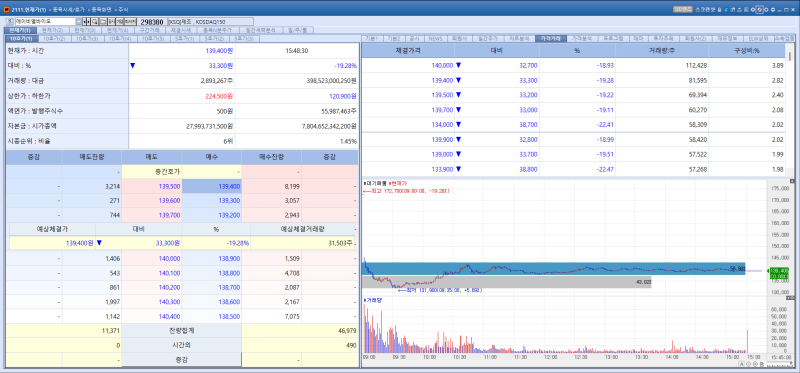

ABL Bio stock trend on Apr 29.(Image=MP Doctor)

◇ABL Bio Falls as Phase 2/3 Results for Bile Duct Cancer Therapy Disappoint

According to KG Zeroin’s MP DOCTOR, ABL Bio’s shares plunged 19.28% from the previous session to close at 139,400 won on the 28th. The decline appears to have been driven by disappointing Phase 2/3 results for ABL001, a bile duct cancer drug candidate out licensed in 2018 to U.S.-based Compass Therapeutics (formerly Trigr Therapeutics), particularly its failure to meet the overall survival (OS) endpoint.

According to Pharm Edaily, a premium biotech content service by Edaily, Compass Therapeutics on March 27 (local time) announced follow-up data from the Phase 2/3 COMPANION-002 trial of tobevibart in patients with bile duct cancer. The dataset included secondary endpoints progression free survival (PFS) and overall survival (OS) following the primary endpoint disclosed in April last year.

Previously, the primary endpoint, objective response rate (ORR), was reported at 17.1% in the treatment group (paclitaxel plus tobevibart) compared with 5.3% in the control group (paclitaxel monotherapy), with a p-value of 0.031.

Compass highlighted PFS as a key achievement in the study median PFS was 4.7 months in the treatment group versus 2.6 months in the control group, with a hazard ratio (HR) of 0.44. The p-value was below 0.0001, indicating statistical significance and a 56% reduction in the risk of disease progression compared to paclitaxel alone. However some analysts noted that the absolute gain of 2.1 months may limit its clinical relevance.

In contrast, OS results were unfavorable. In the intent to treat (ITT) population median OS was 8.9 months in the treatment group and 9.4 months in the control group. The HR was 1.05 with a p-value of 0.78, failing to achieve statistical significance. Compass argued that the OS outcome was confounded by crossover, as 31 out of 57 patients (54%) in the control group switched to the treatment arm.

Among crossover patients, median OS reached 12.8 months, compared with 6.1 months for those who did not cross over. Compass also stated that pooled OS based on treatment exposure was 8.9 months, representing an improvement of about six months over conventional chemotherapy.

Market sentiment toward the data was negative. Compass Therapeutics’ stock plunged by as much as 80% in pre-market trading and remained down about 60% during regular trading.

In response, ABL Bio said in a statement that “the recent share price decline following the ABL001 announcement is an excessive reaction unrelated to the company’s fundamentals,” adding that “there have been no changes to our ongoing core businesses or clinical programs.”

The company also emphasized positive signals in the trial. “ABL001 demonstrated improved survival outcomes across key endpoints, including ORR, PFS and OS, in the treatment group.”

the company said adding that it plans to proceed with the regulatory approval process based on these findings.

NGeneBio stock trend on Apr 29.(Image=MP Doctor)

◇NGeneBio Plunges on Capital Increase and Capital Reduction Plan

NGeneBio’s shares tumbled 25.53% to close at 1,225 won on the day, weighed down by news that the company plans to simultaneously pursue a capital increase and a capital reduction.

The company announced that its board of directors had approved a rights offering of 7.15 million common shares, aiming to raise approximately 22.4 billion won. Of the proceeds, around 17.3 billion won will be used for operating expenses, while 5.1 billion won will be allocated to debt repayment. The offering will be conducted through a shareholder allotment with unsubscribed shares offered to the public.

In parallel, NGeneBio will implement a capital reduction without compensation to offset accumulated losses. The reduction ratio is 66.67%, meaning three existing shares will be consolidated into one. As a result, the total number of outstanding shares will decrease from 26,809,750 to 8,936,583. The record date for the capital reduction is set for June 24, with the listing of new shares scheduled for July 13.

The market viewed the move cautiously. While capital reduction is typically aimed at improving the balance sheet, the subsequent capital increase is expected to dilute existing shareholders’ equity, putting downward pressure on the stock.

NGeneBio explained that the capital increase is a strategic decision to strengthen its financial structure and advance its growth engine centered on an AI-based precision medicine platform, leveraging its next generation sequencing (NGS) diagnostic technology.

The funds raised will be used in a balanced manner to enhance core technologies, expand partnerships with medical institutions, and repay debt to improve financial stability.

According to its investment plan, a significant portion of the funds will be directed toward expanding its AI-driven precision medicine platform. This includes research and development to improve genomic analysis efficiency, upgrading AI-based software capabilities, and building as well as advancing its in hospital genomic information management system (NGLIS).

Through these efforts the company aims to broaden its reach across domestic and global healthcare institutions and establish a high value business model by converting accumulated data into revenue from analytical services.

Part of the funding will also be used for debt repayment to reduce financial costs and enhance balance sheet stability, laying a stronger foundation for mid to long term growth the company said.

An NGeneBio official stated, “This fundraising marks a critical turning point for us to leap forward as a leader in AI-driven precision medicine platforms by integrating AI with medical data, while fundamentally addressing financial risks. We will ensure transparent and efficient use of funds to achieve visible revenue growth and improved profitability, and to rapidly expand our market share in the precision medicine sector.”

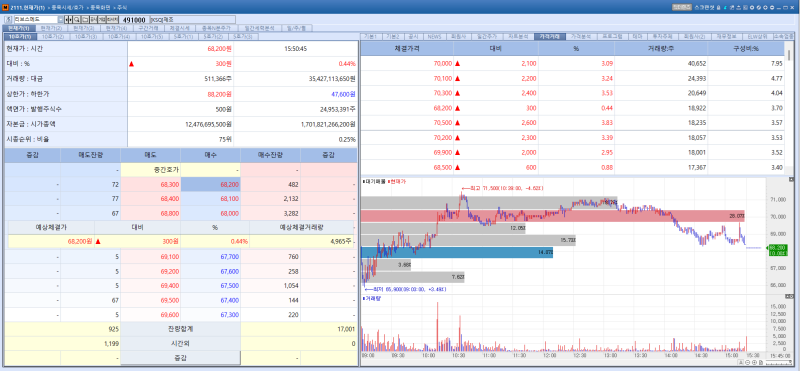

LivsMed stock trend on Apr 29.(Image=MP Doctor)

◇LivsMed Gains on Product Expansion and Global Push

LivsMed’s shares rose 0.44% from the previous session to close at 68,200 won, extending gains for a fourth consecutive trading day since the 23rd. Investor sentiment was supported by expectations that the company will accelerate earnings growth this year through an expanded product lineup and a full-scale push into overseas markets.

The company plans to actively expand abroad with its flagship products, including the articulating laparoscopic instrument ArtiSential and the articulating vascular stapler ArtiSeal. In addition, LivsMed is set to launch new products such as the surgical stapler ArtiStapler and the laparoscopic camera LivsCam.

In particular, LivsMed is expecting meaningful progress in the U.S. market for ArtiSential this year. In April last year, the company signed a supply agreement with HealthTrust, the largest group purchasing organization (GPO) in the U.S. healthcare sector. GPOs evaluate and approve pricing, quality, clinical data, and contract terms on behalf of their member hospitals.

Given that the agreement with HealthTrust was signed in the first half of last year, U.S. sales contributions are expected to be reflected gradually this year. In its securities filing, LivsMed projected revenue of 150.7 billion won for this year, along with a return to operating profit. It also forecast rapid growth to 321.2 billion won next year and 564.8 billion won by 2028.

The company is also aiming to obtain regulatory approval from Korea’s Ministry of Food and Drug Safety this year for its surgical robot, Stark.

A LivsMed official said, “Last year marked a significant milestone for the company, with strong revenue growth, improved profitability, and the completion of a new product portfolio. These achievements are not just the result of a single year, but the culmination of efforts to build a solid foundation for explosive growth going forward.”

The official added, “With the full scale launch of new products and the ramp up of sales for the Stark surgical robot, we aim to achieve both qualitative and quantitative growth and reward the trust of our investors.”